Experts discuss Western Australia’s industrial property market

Hundreds of people tuned in to listen to the 25th edition of RWC’s Between the Lines webinar today, where our panel of experts discussed Western Australia’s industrial market.

Over the past decade, the childcare sector has experienced significant growth within the alternative commercial property market. The affordability of these assets has made them appealing to private investors. However, the sector has become more sophisticated with the emergence of funds, syndicates, and larger groups seeking to take advantage of this heavily subsidised income stream. Before the pandemic, there was a rapid increase in development activity in this area, particularly on the east coast, with approval and consent levels rising as many owners sought to capitalise on the growing demand.

Due to rising construction costs in recent years, many of these sites have not been developed, and these approvals may expire as concerns grow about the relative demand for additional childcare space across the sector. Australia continues to experience strong population growth, however, this does not necessarily translate into childcare demand. The influx of overseas migrants and their families has led to a cultural shift in some areas, resulting in changing occupancy fundamentals for the asset.

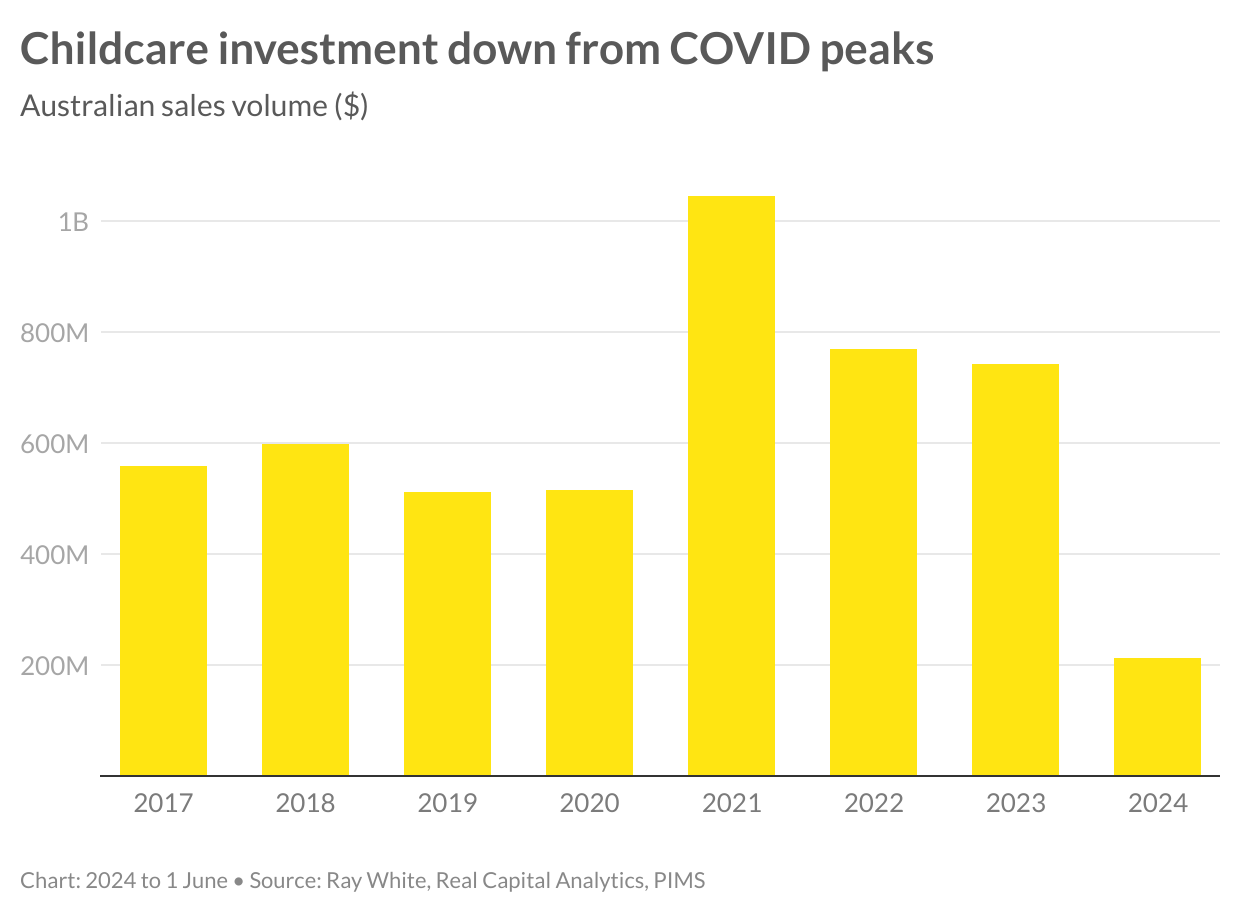

It is evident that the performance of childcare centres remains dependent on their location. The federal government’s ongoing support through subsidies and the education of early childcare workers highlights the sustained demand for these facilities. In 2023, childcare centre transactions across Australia totaled $743 million, representing a 3.4 percent decrease from 2022 results and a 28.9 percent decline from the market peak in 2021, when buyers took advantage of low-cost financing and the trend towards greater portfolio diversification. The first five months of 2024 have seen just over $200 million in sales, with a strong emphasis on metropolitan assets. Transaction volumes are evenly distributed across NSW, Queensland, and Victoria. There has also been an increase in the number of sites coming to the market as they become increasingly challenging to “stack up” in the current economic environment.

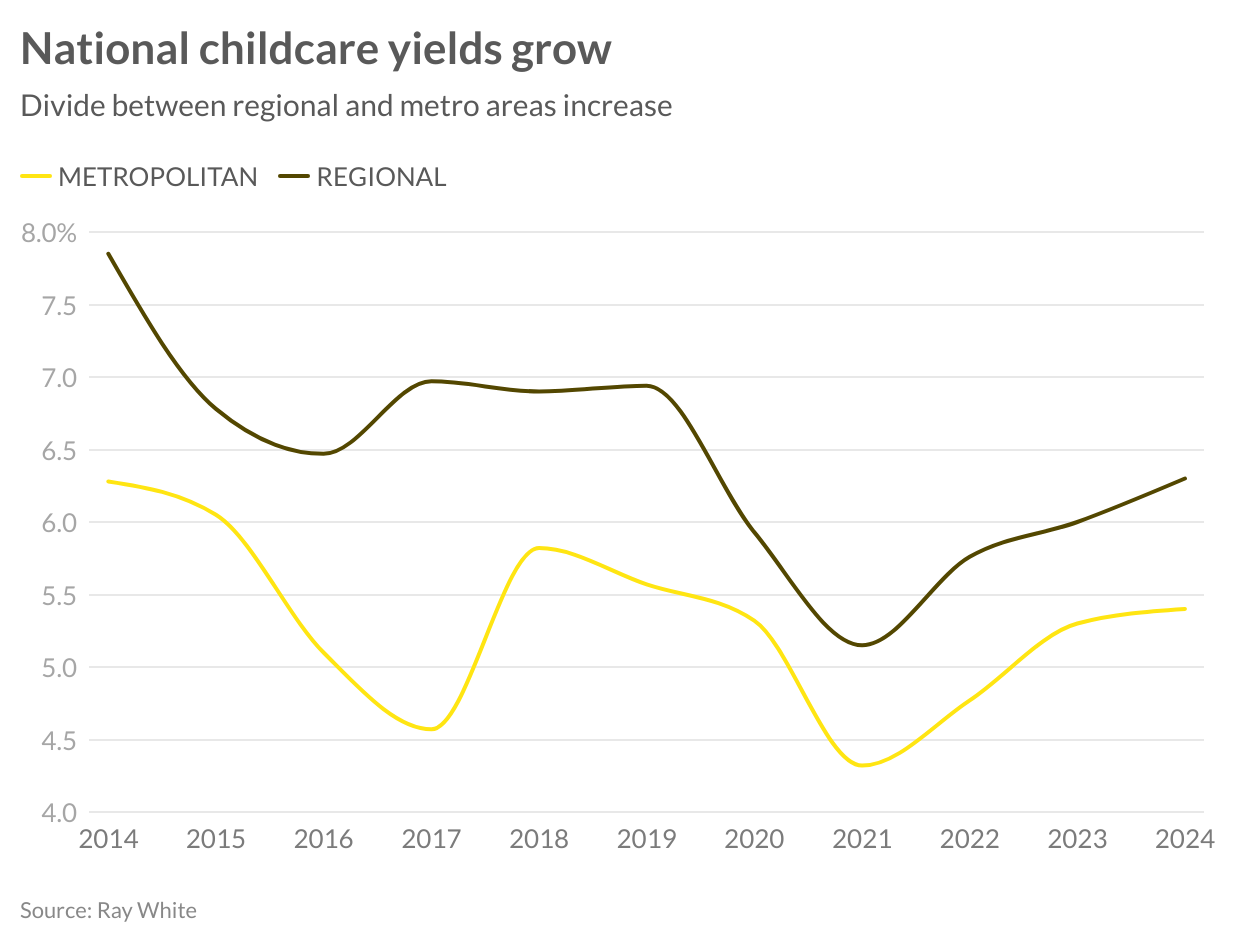

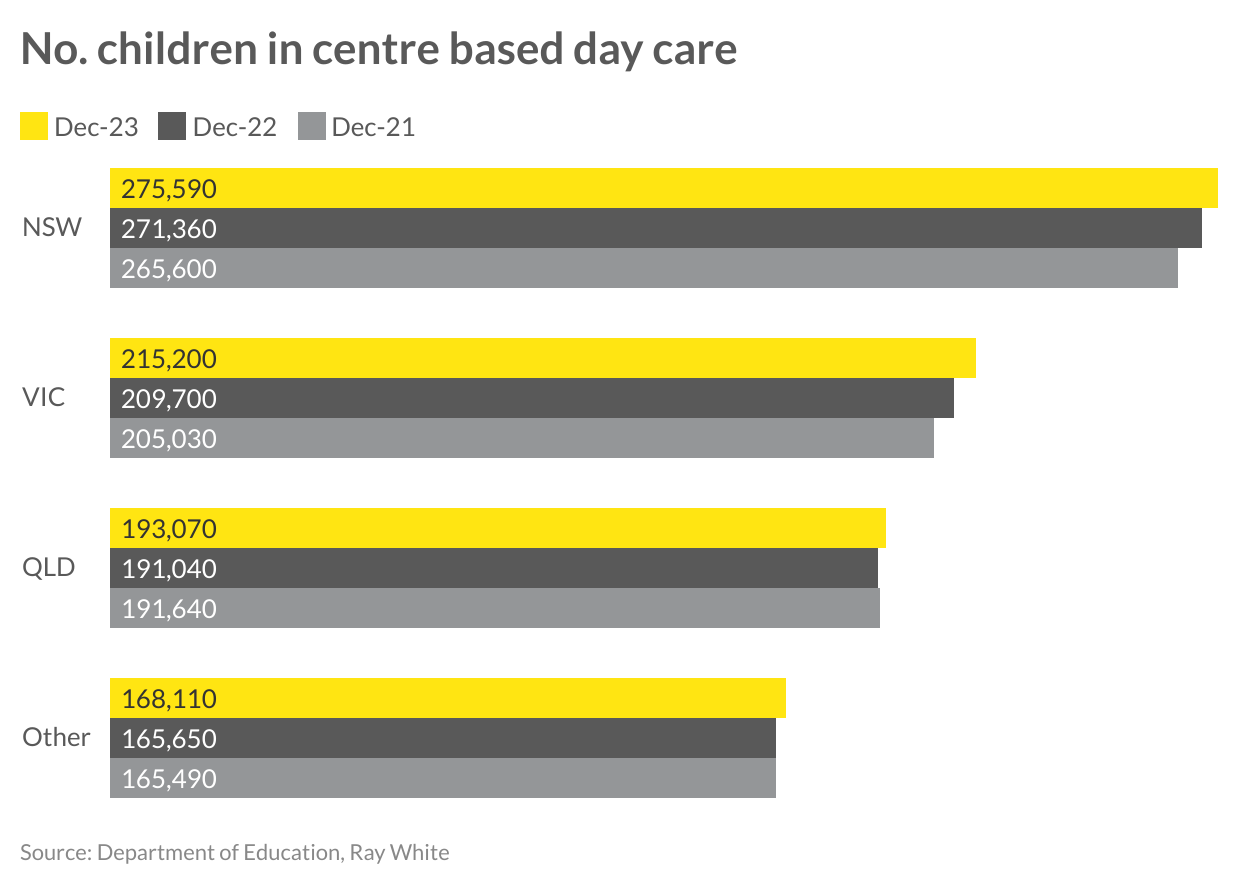

Yield results have been mixed, with rates increasing since 2022 due to higher financing costs. However, the gap between metropolitan and regional assets has widened as buyers become more cautious and considerate of occupancy trends. Average metropolitan yields remain below 5.5 percent, with some sales this year as low as 4.8 percent, rivalling many other more established property asset classes. With the average sale price across the country remaining below $5 million, childcare centres continue to be an accessible investment option for the growing number of investors looking to expand their portfolios with commercial offerings.The childcare sector’s fundamentals remain positive, with data from the Department of Education showing a consistent increase in the number of children attending day care. Victoria leads the way with a 2.6 percent increase in the 2023 calendar year, although NSW has the highest number of children in childcare compared to other states. Moreover, the average number of hours children spend in childcare continues to rise, currently at 33.3 hours per week per child, up from less than 30 hours in 2019. Coupled with a 16 percent increase in the hourly rate paid for childcare over the past two years, now at $12.35, it’s clear why investing in childcare is an attractive option.

However, affordability remains a concern for many families, and several state governments are working to provide assistance through subsidies and expanded public preschool offerings, which could compete with many childcare providers. For investors, thorough location research is crucial to understanding the long-term viability of a childcare investment, not just considering potential population growth. Competition and new development can impact occupancy, but the fundamentals of childcare as a stable, income-generating asset class remain sound.

By Vanessa Rader | Head of Research

Hundreds of people tuned in to listen to the 25th edition of RWC’s Between the Lines webinar today, where our panel of experts discussed Western Australia’s industrial market.

The Perth retail strip market has seen a notable uptick in occupancy across the eight surveyed areas.