Experts discuss Western Australia’s industrial property market

Hundreds of people tuned in to listen to the 25th edition of RWC’s Between the Lines webinar today, where our panel of experts discussed Western Australia’s industrial market.

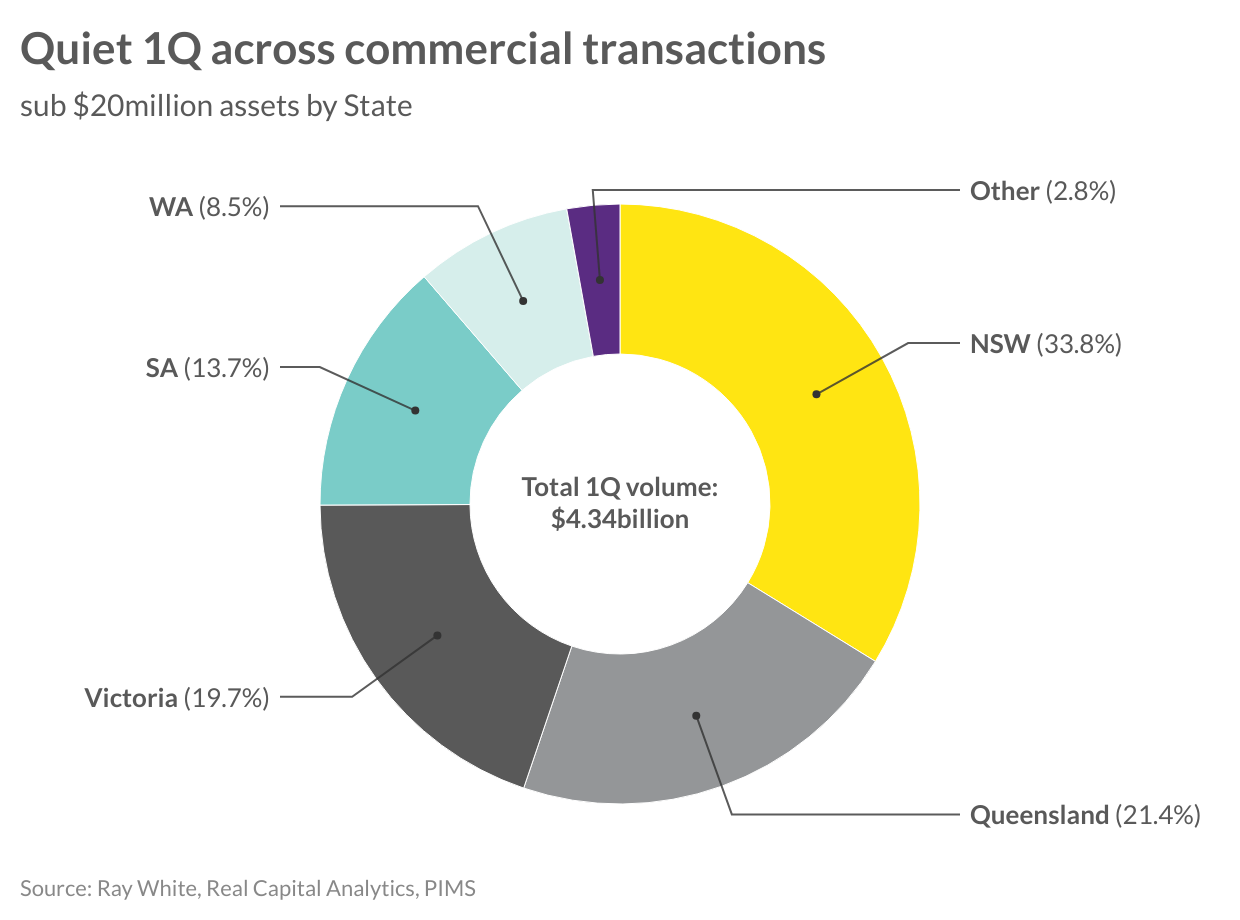

The commercial property market has had another quiet start to the year, recording its third consecutive reduction in first quarter results. In 2024 we have commenced the year turning over $4.34 billion across the sub-$20 million market, down 48.6 per cent on the same period in 2023 after falling more than 30 per cent the prior year. Uncertainty surrounding the economy has been the key factor keeping transaction levels subdued with many buyers and sellers anxiously awaiting the next interest rate move. Encouragingly, the latest inflation results have shown continued downward momentum, albeit not falling as rapidly as anticipated. However, sentiment surrounding interest rate reductions is maintained for later this year, which will likely result in an uptick in sales volumes, notably across the smaller end of the market.

Private buyers continue to actively pursue quality assets across the country, with NSW the premier location for investment, recording approximately a third of all sales. Queensland has overtaken Victoria as the second most popular destination for investment capital (sub $20million) supported by strong population and economic gains across the greater south east Queensland region. After recording more than a quarter of all sales during Q1 2023, Victoria has felt a reduction in investment activity to represent less than 20 per cent. Similarly, Western Australia’s share of sales in the sub-$20 million price point is down from 10.8 per cent in Q1 2023 to 8.5 per cent this year. Activity across the South Australian market has turned a corner during the start of the year recording close to $600 million, representing 13.7 per cent of sales, up from 8.2 per cent last year.

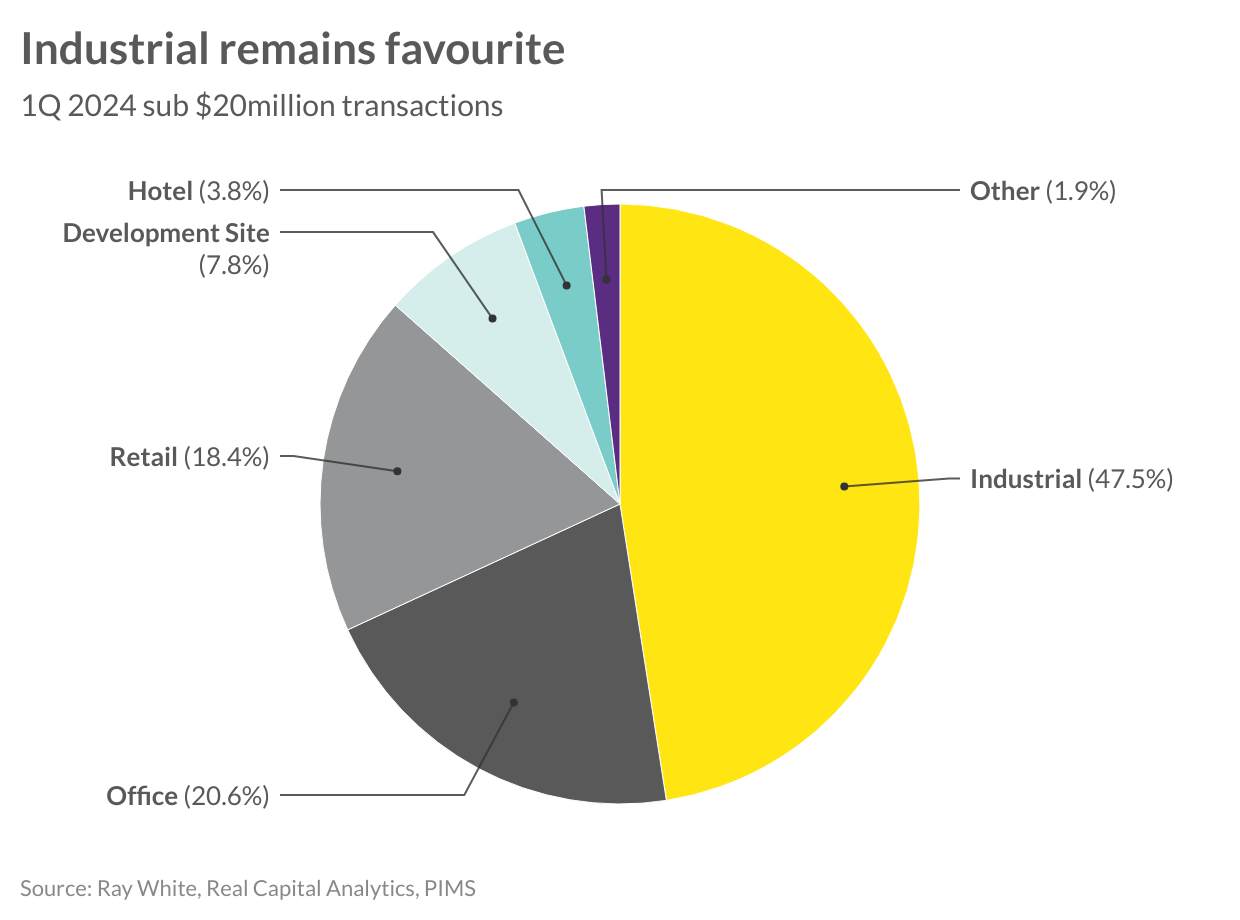

Despite the reduction in overall sales, there is a clear winner for the asset class in greatest demand. Representing over $2 billion, industrial transactions amount to 47.5 per cent of the total volume of sales in the sub-$20 million price point. With assets available in a range of price points, there is strong interest by both private investors and owner occupiers due to the robust increases in rents over the past few years. Office has maintained a 20 per cent share of the sub-$20 million pool of investment over the last three years, with high vacancies and attractive leasing terms on offer, smaller buyers and occupiers have not grown their interest in office assets, however, smaller freehold assets have been popular in some markets.

While retail has only accounted for 18.4 per cent of sales early this year, across the total commercial investment market we have witnessed a resurgence in confidence across the retail sector. There has been a strong increase in transactions for convenience, neighbourhood and sub-regional centres off the back of price corrections and population increases. Activity across development sites has also trended up and “other” assets such as childcare, medical, and blocks of units continued to be in hot demand by private buyer groups looking for attractive, long-term returns.

While activity has been subdued for the first quarter this year, limited quality stock has been a major hurdle for those looking to invest. The anticipation of interest rate movements has brought more buyers into the market this year than previous years, particularly given the price and yield corrections which have been felt across all asset types. The sub-$20million price point is accessible to a larger pool of investors and as such we are expecting to see activity levels rebound and volumes to be back on track to exceed 2023 results.

By Vanessa Rader – Head of Research

Hundreds of people tuned in to listen to the 25th edition of RWC’s Between the Lines webinar today, where our panel of experts discussed Western Australia’s industrial market.

The Perth retail strip market has seen a notable uptick in occupancy across the eight surveyed areas.